Share this Article

The highly anticipated Consumer Financial Protection Bureau (CFPB) Debt Collection Town Hall will be taking place Wednesday, May 8, in Philadelphia. It is expected that this event is where the Bureau will release new proposed rules for debt collection.

In preparation for the Town Hall, AccountsRecovery.net held a webinar on the topic. Joann Needleman, Mike Frost, Scott E. Wortman, and John Bedard gathered to discuss how the credit and collections industry got to this point, what impact the rules may have on agencies, and what comes next once the proposed rules are released.

Why Have The New Debt Collection Rules Taken So Long?

Needleman began the panel by discussing the long road that has led us to the present. The Bureau was created almost a decade ago, and spent much of the early years requesting and reviewing information in order to move forward with regulation.

Most ARM industry professionals know a rule was originally meant to be proposed in late 2017. After then-Director Richard Cordray stepped down from his post, replaced by acting director Mick Mulvaney, the proposed rule release was cancelled. Since then, a new director, Kathleen Kraninger has been confirmed. These many changes throughout the last few years has delayed the rule proposal, and perhaps created a more favorable outcome for more balanced, clear guidelines under Kraninger.

The overturn in leadership wasn’t the only reason for delay. “There are a lot of stakeholders with a lot of concerns,” says Bedard. The CFPB originally received thousands of comments about the industry shortly after its creation. Sifting through this immense amount of information and thoughtfully applying it to future work took time.

Call Caps

Kraninger noted in a speech last month that the upcoming rules will contain guidelines for how many calls per week a consumer may receive. In the webinar, Wortman discussed some states that already attempt to limit the number of communications collectors may have with consumers.

The FDCPA doesn’t specify how many times a collector may call a consumer (although it prohibits using calls as an annoyance or harassment tool). In a few states where call caps are already present some language refers to “communication” in place of calls, leaving the subject vague. A more specific call volume cap can potentially be a positive change to make right party contacts more efficient.

The concern many ARM professionals have with call caps is that every type of debt collection agency is different. A one-size-fits-all approach does not work when collection tactics differ based on the type of debt and even between agencies. Caps across the board could leave agencies trying to adapt and even make their businesses less efficient.

Related Article

Text and Email Use

One of the more anticipated topics to be covered is the use of text and email as acceptable forms of communication. Many debt collectors want to update business practices by using text and email to interact with consumers. The rules surrounding text and email don’t expressly address the issue. Many are hoping for clear, specific language to help collectors easily comply with regulations while using updated technologies.

The panel spoke about the attention text and email use is getting from consumer advocates. These consumer groups are expressing concern for wider adoption of technology in fear of burdensome contact from collectors. However, as Frost pointed out, many recent studies actually suggest millennials and other young consumers have shown growing preference for text and email over telephone communication.

Bedard hopes clarification in the proposed rules will be specific enough to help agencies comply easily and decrease the need to rely on courts to weigh in on the subject.

What is the Debt Collection Rule Proposal Process?

The process the CFPB follows is to present the proposed rules for public review. At that point, the CFPB will specify a comment period, during which, any interested party may provide their feedback on the rule contents.

After this period ends, the bureau will review all of the comments received before proceeding to finalize the rule. Before their release, the Bureau will make a statement on how the comments received impacted the final rules. The panel explained that there are a few different possibilities at the time the final rules are presented.

If the final rules are similar to the original proposal, the Bureau will simply provide a date the rules will go into effect, giving time for all businesses to prepare to comply. However, if the final rule is wildly different from the proposed rule, there is potential for a second comment period at that point, drawing things out further.

The process takes anywhere from many months to more than a year to complete. It’s likely the industry won’t see a finalized change until 2020 or even 2021.

Related Article

Why is Industry Participation Important?

All four panelists stressed that participating in cfpb proposed rules process is the only way to gain the regulatory clarity the ARM industry has craved. By reviewing the proposed rule and making detailed comments on how it will impact you, your agency will be creating lasting change for yourself and your peers.

Submitting comments is also important to create a written record of your opinion as a member of the industry.

There is nothing at present to indicate the proposed rules will appear arbitrary, but as Needleman points out, there is no going back to create these materials later. It is better to speak up now, while you have the chance.

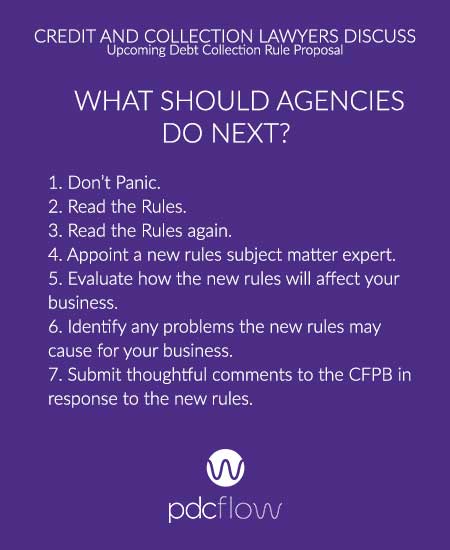

What Should Agencies Do Next?

The first step the panel agreed upon - don’t panic! It is important to remember that this is simply one step in a longer process.

Appoint someone within your agency to serve as the subject matter expert on these rules, but don’t enact any changes at this stage. Evaluate what the rules would mean in relation to you. Identify any problems the rules would cause within your business and use those as talking points to add to your CFPB comments.

PDCflow will be following the newest developments to keep you informed. To stay up-to-date on the CFPB’s proposed debt collection rules, and other educational collection industry content, subscribe to the PDCflow blog: